Performance and investments of unlisted real estate funds in the first half of 2022

ASPIM and IEIF have published performance and investment statistics for unlisted real estate funds in the first half of 2022.

Performance in the first half of 2022

Payout and valuation of SCPIs still on the rise

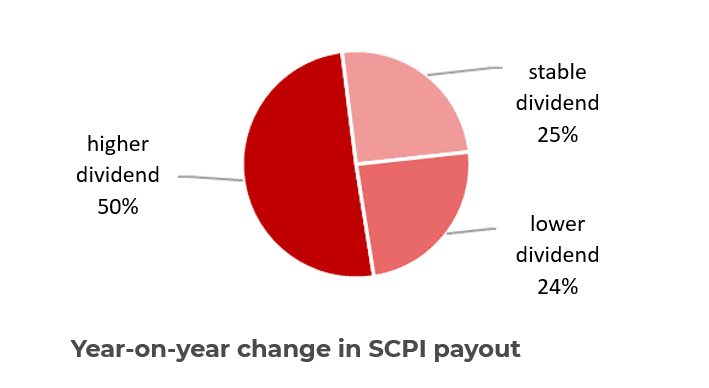

Dividends paid for the first half of 2022 increased by a capitalisation-weighted average of +4.3 % compared with the first half of 2021. Looking at the detail, 50% of SCPIs by number paid higher interim dividends that increased year-on-year (+13% as a weighted average), 26% of SCPIs paid stable interim dividends and 24% of SCPIs paid lower interim dividends (-3% as a weighted average). Based on the reference price at 1 January, the average payout ratio of SCPIs, all categories combined, was 2.15% in the first half of 2022.

SCPI share prices increased by a weighted average of +0.7% in the first half of 2022. In detail, share prices remained unchanged for 72% of SCPIs in number, and 25 % of SCPIs recorded price increases (+2.6% as a weighted average). Lastly, only 3% of SCPIs recorded a price decline (-1.8% as a weighted average). Given the current context of high inflation and rising interest rates, managers are cautious about the trend in appraisal values at the end of the year.

Market averages are in line with the EDHEC IEIF France real estate price index,[1] which indicates an overall performance of 2.8 % since 31 December 2021[2].

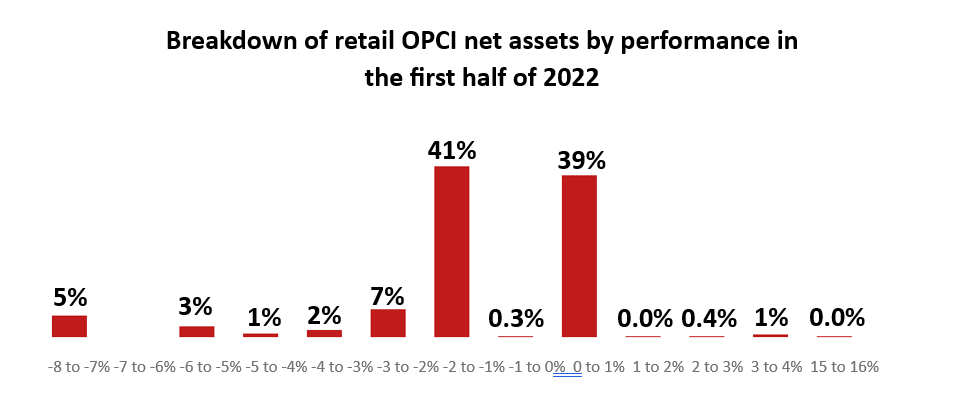

Retail OPCI performance hurt by the financial segments

39% of the market delivered an overall performance of between 0% and +1% in the first half of 2022 (source: ASPIM)

The average overall performance of all retail OPCIs was -1.4% in the first half of the year (compared with +0.4% at the end of the first quarter). The fall in the financial markets in the second quarter was the reason for the underperformance of the financial and listed real estate segments of retail OPCIs. The IEIF REIT Europe index fell by -18.8% in the second quarter (compared with -0.2% in the first quarter). This negative performance of the financial segments was nevertheless offset by the increase in the appraised value of real estate assets and the good level of rental income in the first half of the year.

As of 30 June 2022, the net assets of the 23 retail OPCIs stood at €20.7 billion.

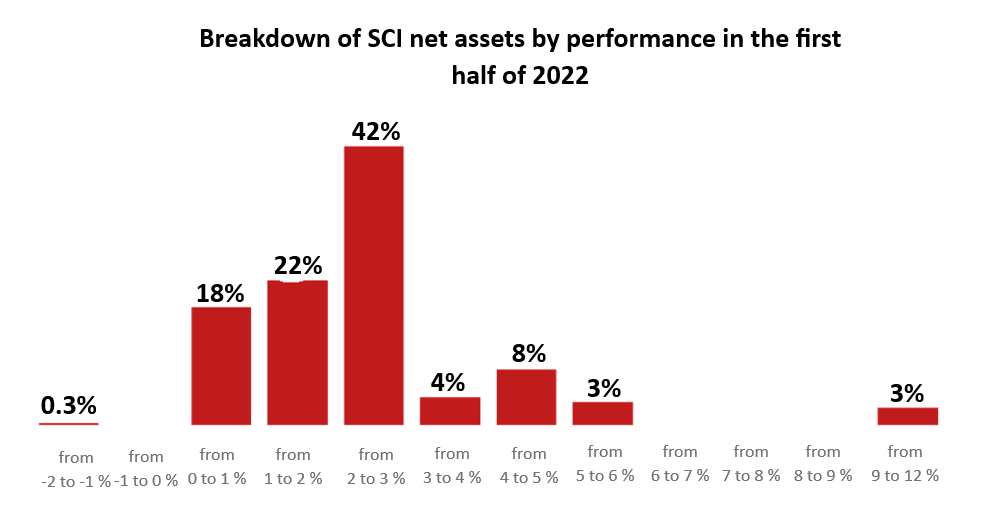

The performance of unit-linked SCIs (non-trading real estate companies) was +2.6% in the first half.

42% of the market delivered an overall performance of between +2% and +3% in the first half of 2022 (source: ASPIM)

In the first half of 2022, unit-linked SCIs delivered an overall performance of +2.6%.

As of 30 June 2022, the net assets of the 37 unit-linked SCIs stood at €21.7 billion.

Investments in the first half of 2022

In the first half of 2022, real estate acquisitions by the three categories of retail funds totalled €5.6 billion. In detail, SCPIs made acquisitions worth €4.6 billion. SCIs invested nearly €800 million in direct real estate, or 40% of their total investments in the first half (€2 billion). In addition to direct real estate, shares in unlisted real estate funds accounted for 47% of the total allocation of SCIs in the first half of the year (of which 25% in SCPIs). Lastly, acquisitions by retail OPCIs amounted to around €250 million.

In terms of disposals, the three categories of retail funds sold around €800 million worth of assets, including €540 million in asset disposals for SCPIs.

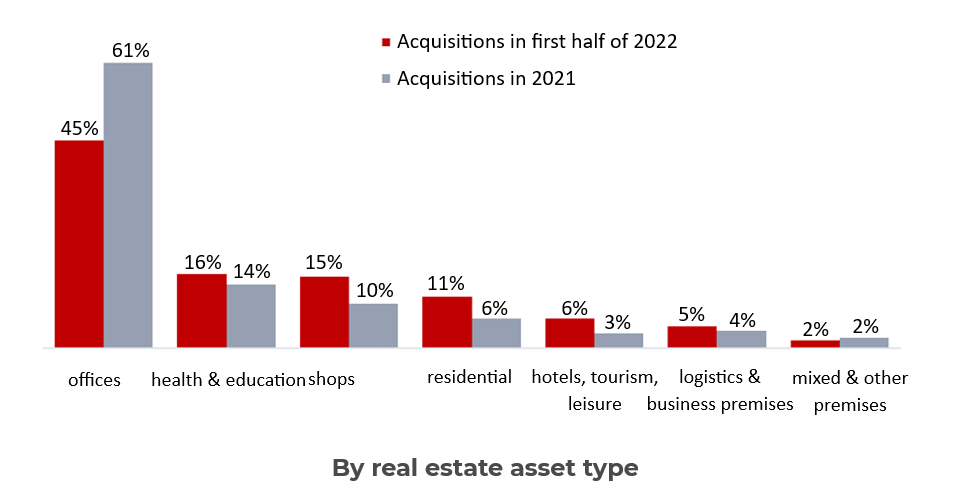

In terms of asset type, offices accounted for 45% of the acquisitions made in the first half of 2022, followed by health and education (16%), shops (15%), residential (11% including managed residences) and hotels and leisure (6%). Lastly, logistics and business premises accounted for 5% of amounts invested.

Asset disposals in the first half of the year were primarily in offices (69%), followed by shops (14%), residential (6%), hotels and leisure (5%), logistics and business premises (3%) and lastly health and education (3%).

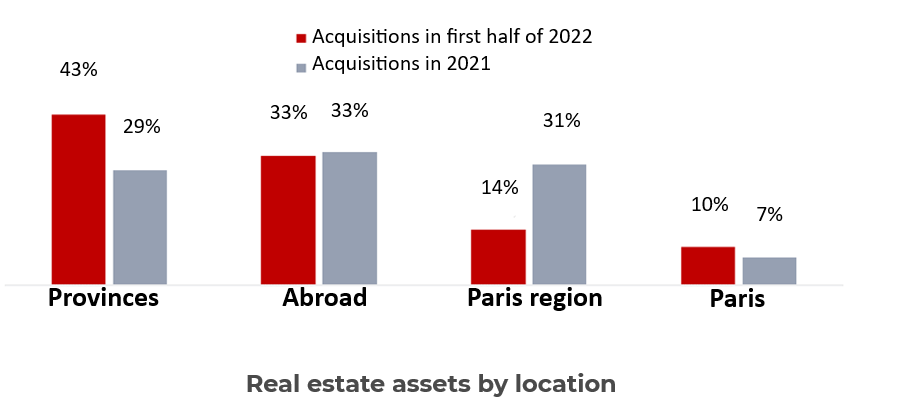

In terms of location, the largest amount of investments was made in the regions (43 %), then abroad (33 %) and lastly in the Greater Paris region (24 %, including 10% in Paris).

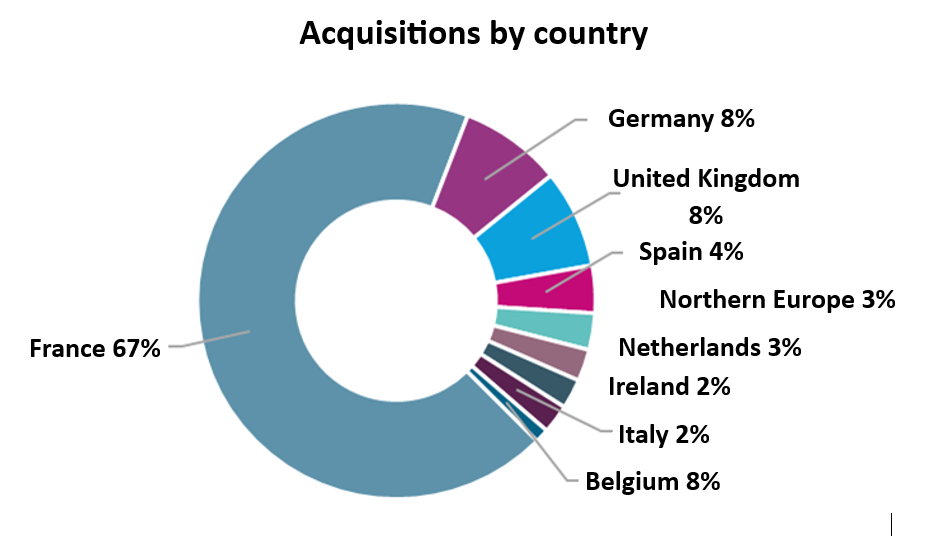

Outside France, Germany (8%) was just ahead of the United Kingdom (8%), followed by Spain (4%), Northern Europe (3%), the Netherlands (3%), Ireland (2%), Spain (2%), Italy (2%) and Belgium (1%).

Regarding disposals, 52% of the assets sold were located in the Greater Paris region (including 34% in Paris), 25% abroad and 23% in the regions.

[1] Index composed of fixed and variable capital SCPIs that reported more than €2 million in trading volumes on the secondary market during the previous year.

[2] Including 2.1% current yield and +0.7% valuation